Tax Free!

That’s Right, QCDs are Tax Free!

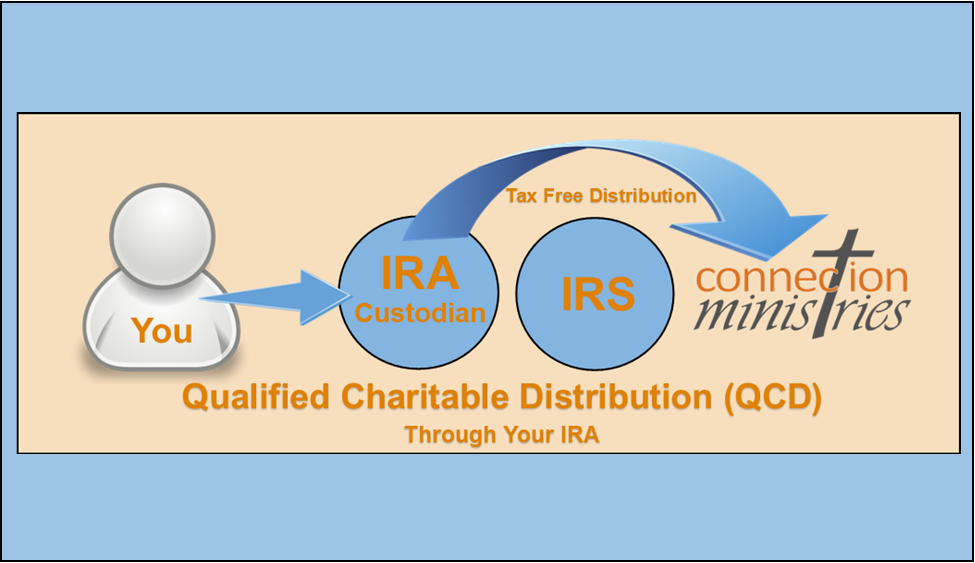

Did you know that you can support charities like Connection Ministries directly from your IRA tax free?

For individuals who are 70½ and charitably minded, the strategy outlined in this “Illuminate Blog” can offer valuable tax advantages. It’s called a Qualified Charitable Distribution or QCD. However, as with any financial or tax strategy, it’s best to understand the details and limitations and talk with your tax advisor.

A QCD is a tax-effective way to support your causes, especially if you don’t itemize your deductions. If you plan to take an IRA distribution, whether it is for a Required Minimum Distribution (RMD), or another reason, and you also plan to make charitable gifts, consider making the charitable gifts from your IRA through a QCD. Your charitable gifts through a QCD are tax free. In effect, you receive a value that is better than a tax deduction.

Receiving a normal distribution from your IRA could increase your taxes in several ways whether it is for an RMD or not.

- Since normal IRA distributions are considered ordinary taxable income, it can push some retirees into a higher marginal tax bracket.

- IRA distributions also increase the taxpayer’s modified adjusted gross income, or MAGI, which could trigger the 3.8% Medicare surtax. Large distributions can also impact Medicare Part B and D premiums.

- Even modest IRA distributions can cause Social Security benefits to become taxable, up to 85%

You can use any portion of a planned IRA distribution as a QCD to make your charitable gifts, without increasing your ordinary taxable income.

Here are a few details you should consider.

- You must be at least 70½ years old at the time you request a QCD.

- For a QCD to count towards your current year’s RMD, the funds must come out of your IRA by your RMD deadline, generally December 31.

- Your IRA custodian must transfer the funds directly to the qualified charity. If a distribution check is made payable to you, the distribution would NOT qualify as a QCD and would be treated as taxable income.

- The maximum annual total distribution amount that qualifies for QCDs in a calendar year is $100,000. If you’re married filing jointly, both you and your spouse can each contribute up to $100,000 in QCDs from your own IRAs.

QCDs are not considered taxable income and therefore people over age 70 ½, who intend to be charitable with 501(c)(3) organizations like Connection Ministries will find the QCD worth considering.